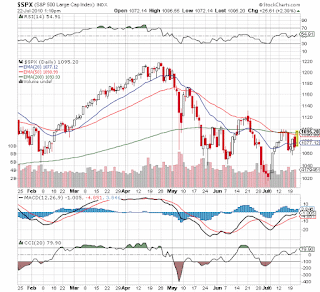

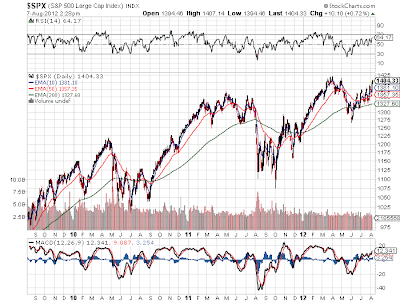

Market Approaching 4 Years Highs

Quick, how many people expected the stock market to surge towards multi year highs at the start of August? The very time period where the market nearly fell off the cliff last summer. Even as the European issues continue to mount, it finally appears that the market has gotten past the never ending financial crisis. Not to mention that earnings report after earnings report provided solid numbers. Is the market finally able to focus on company specific events or will it be right back to the nuances in Europe as the Olympics end? In fact, maybe the Olympics have only hidden the issues as the world focuses on sporting events instead of financial issues. Don't be surprised to see next week bring out some fear mongering stories. For now, if your in the stock market just sit back and enjoy the gains while the average person is sitting on the sidelines watching stocks soar. 3 Year Chart - S&P 500 Disclsoure: No positions mentioned. Please review the d...