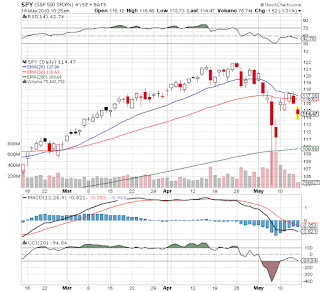

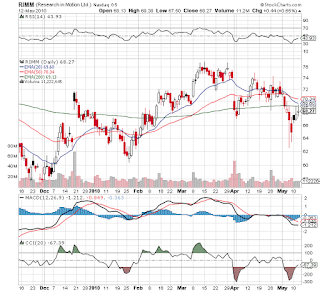

Trade: Bought Massey Energy, China Armco Metals; Covered Research in Motion

Postings have been slow of late because of moving into a new house. Regardless, we've been focused on taking advantage of the drop in the market. Yesterday, the Opportunistic Portfolio bought Massey Energy (MEE) and China Armco Metals (CNAM) and covered the short on Research in Motion (RIMM). Unfortunately besides a small short on RIMM, we missed reducing exposure on the drop, but we're confident that we picked up MEE and CNAM on the cheap yesterday. Last check that portfolio is up nearly 8% today. The basic theme was to buy what China needs and the met coal from MEE and the recycled steel from CNAM were the just the ideal options. It doesn't hurt that the stocks are down 40-60% from recent highs. Its become evident that China is going to protract any rate hikes due to the issues in Europe and hence the market is likely to flock back into the China theme which means more commodities. More on this subject later.