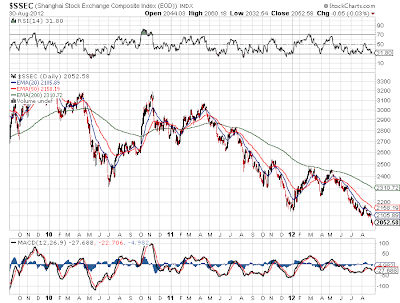

Shanghai Composite Keeps Falling To New Lows

Amazingly the China stock market as represented by the Shanghai Composite keeps to new multi-year lows. As seen from the below 3 year chart, the index as virtually fallen every month since the peak back in October 2011 at nearly 3,200. The index is now barely holding onto 2,000 after a very weak summer. Ultimately this should lead to more stimulus eventually. Investors should keep an eye on a bottom for the coal producers or other mining stocks that have been crushed this year. China has clearly slowed down, but the question still remains whether growth will be 6% or 8% which is a far cry from a recession. Disclosure: No positions mentioned. Please review the disclaimer page for more details.