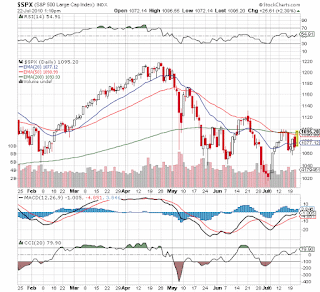

Stat of the Day: Chicago PMI Backlog and New Orders Jump

As everybody frets over a soft patch in the US economy and the backward looking Q2 GDP report today, the Chicago PMI for July came in at a very robust 62.3. A full 6 points above the 56 consensus and even 4 points above the most optimistic economist at 58.4. The markets initially sold off based on the GDP report, but some sanity has returned after the Chicago PMI. Actually the market is still somewhat acting like a lunatic considering the GDP report should be meaningless and the Chicago PMI + earnings reports are so bullish that the market should be soaring today. Why does the market even care about the GDP report? Do we now go back and adjust the terrific earnings reports of Intel (INTC), Caterpillar (CAT), or FedEx (FDX) because GDP was weak? Does it in any way impact guidance? The answer is a resounding NO! Besides, most of the SP500 doesn't even rely on the US for growth anymore. Back to the Chicago PMI. New orders came in at a robust 64.6 with backlog jumping 7 points to 57.6....