Zynga: Disappointing Deal Value

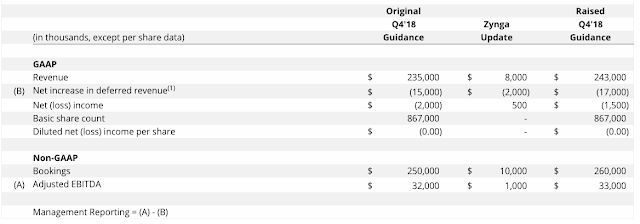

Zynga agrees to be bought by Take-Two Interactive at a disappointing valuation despite the deal premium. The new entity proposes a company rivaling EA trading at a major discount to the gaming giant. The new Take-Two will have appealing 14% growth rates plus $500 million in net bookings synergies in mobile. The stock will trade at a FY23 EV/S multiple of 3.5x, which is a major discount to past multiples. This idea was discussed in more depth with members of my private investing community, Out Fox The Street. Learn More » For long-term shareholders, the Take-Two Interactive Software ( TTWO ) deal to acquire Zynga ( ZNGA ) for $10 per share is a disappointing valuation considering the stock regularly traded above $11 last year. For short-term traders, the 64% premium provides a good time to exit the stock after a rough last few months. My investment thesis remains Bullish on the stock after the massive hit to Take-Two Interactive takes Zyng...