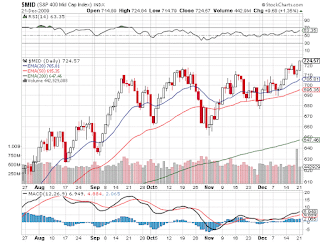

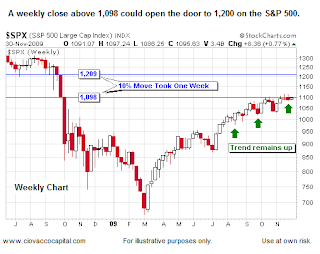

Buy & Hold for the Next Decade

Interesting discussion with Vince Farrell about how the Buy & Hold method might have been the wrong strategy in the last decade, but it likely could thrive in the next decade. IMO, anytime a theory is supposedly dead is the time to start using it again. Though I'll say that Buy & Hold as a theory really only works when discussing Mutual Fund investing or ETF indexes. The successful funds never remain with the same stocks and rarely does keeping an individual stock over a extended period profitable. The stock market consistently misprices assets whether too high or low. A good investor will take advantage and switch from the high prices to the low prices stock. Considering the last 10 years was the worst decade for holding stocks, it's only logical that the next 10 years should be strong. You'll note that most people don't agree as they've been rushing into bond funds at record levels. By the way, Energy was the best performing sector up some 600% last decade...