Stat of the Day: Investors Yank More Money From Stock Funds

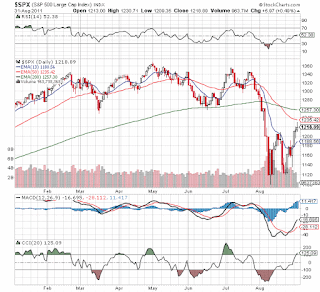

After pulling $34B from US stock funds during the first two weeks of August, the hit parade continued last week with another $3.2B pulled . Not to mention another $610M removed from foreign equity funds for the week ending Aug 24. Note how the SP500 bottomed right in the middle of the frantic selling by retail investors. Now as the market pushes higher throughout August retail investors are still skittish. They are always a great contraian indicator. Disclosure: No positions mentioned. Please review the disclaimer page: