Potential Breakout on Liz Claiborne

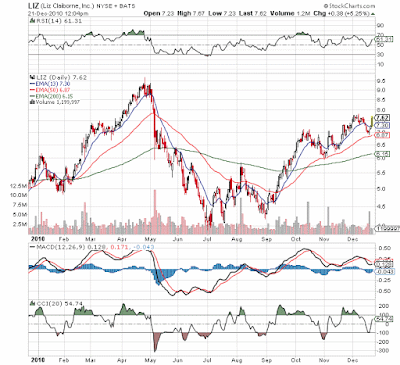

Interesting movement today in Liz Claiborne (LIZ). The company is still struggling to right size its business structure and return to a profitable company. The stock is up over 5% today around the $7.65 area which is close to the recent highs of $7.79 intraday and a closing high of $7.61 just on December 6th. A close at these levels and any follow through tomorrow could signal much higher prices. Not sure what the market is telling us other then the retail environment has been strong this holiday season. Interesting though is that Jones Group (JNY) is only up 1% today and its no where near recent highs in Oct around $21 which is much higher then the current sub $16. Maybe LIZ is in play and thats why the stock has been strong. Regardless the stock is possibly set up for a retest of the yearly highs in the $9-9.5 range reached back in late April. LIZ isn't thought to be well run so somebody apparently knows something to aggressively buy LIZ today. Its a cheap company if they can...