Junk Bond Investors Say Not So Fast

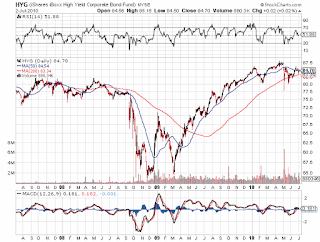

Very odd to the Junk Bond Funds doing so well in the face of a recession. The iShares High Yield Corporate Bond Fund (HYG) has in fact held near recent highs. Much higher then even back in 2007 prior to the collapse of the economy.

What do junk bond investors know that equity guys don't? Surely these bonds would plunge if a double dip was imminent. Why is it holding up better then in mid 2007? Sure corporate profits are strong and the general balance sheet is strong, but these companies wouldn't have junk bonds if they feel into that category. A double dip should be disastrous to such a company.

Stocks of such companies like a Terex (TEX) or Liz Claiborne (LIZ) have just about been annihilated in this selloff but not the bonds of other high yielders? Thought bond traders always knew best.

Non confirmation of the Junk Bond Funds. First, the HYG has hardly budged from recently highs and has easily rebounded from the flash crash lows.

Another similar fund from Braclays (old Lehman) with the symbol of JNK has survived the recent crisis very well. Its even up over the last week and month. Why isn't it confirming the fear in the equity markets? Why are those investors willing to pay up?

So investors are piling into Treasuries pushing 10 year yields down to record levels, but they aren't selling the riskiest of bonds? Doesn't add up and one group will be eventually proven wrong.

What do junk bond investors know that equity guys don't? Surely these bonds would plunge if a double dip was imminent. Why is it holding up better then in mid 2007? Sure corporate profits are strong and the general balance sheet is strong, but these companies wouldn't have junk bonds if they feel into that category. A double dip should be disastrous to such a company.

Stocks of such companies like a Terex (TEX) or Liz Claiborne (LIZ) have just about been annihilated in this selloff but not the bonds of other high yielders? Thought bond traders always knew best.

Non confirmation of the Junk Bond Funds. First, the HYG has hardly budged from recently highs and has easily rebounded from the flash crash lows.

Another similar fund from Braclays (old Lehman) with the symbol of JNK has survived the recent crisis very well. Its even up over the last week and month. Why isn't it confirming the fear in the equity markets? Why are those investors willing to pay up?

So investors are piling into Treasuries pushing 10 year yields down to record levels, but they aren't selling the riskiest of bonds? Doesn't add up and one group will be eventually proven wrong.

Comments